On March 10, Reddit exploded with reports of old City of Ottawa debts mysteriously appearing on credit reports.

Based on reporting from CBC Ottawa, on January 12, 2024, the City of Ottawa signed a five year collection agreement with Financial Debt Recovery (FDR), to collect old accounts, including outstanding parking fines and unpaid water bills.

It is standard practice to hire a collection agency to collect outstanding debts. Collection agencies will use many collection tools to induce payment, including reporting debts under collection to one or both of Canada’s credit bureaus – TransUnion and Equifax.

The way I see it, there are three possible problems with the collection agencies’ approach on behalf of the City of Ottawa.

- Is FDR, the new collection agency, required to send fresh notifications before reporting 103,000 accounts to the credit bureau? I think so.

- The age of the debts appears to exceed the limitation period.

- Many debts were too old to be reported to the credit bureau.

Table of Contents

Notice of debt collection requirements

Under the Regulations to the Collection and Debt Settlement Services Act of Ontario, a collection agent must send a letter to the debtor at least six days prior to commencing collection action (bold by author):

- (1) No collection agency or collector shall demand payment or otherwise attempt to collect payment of a debt from a debtor or in any other way contact the debtor before the sixth day after sending a notice described in subsection (2), except as permitted under subsection (3), section 21.1 or 21.2. O. Reg. 460/17, s. 11.

(2) The notice shall be a private written notice to the debtor setting out the following information:

- The name of the creditor to whom the debt is owed and, if different, the name of the creditor to whom the debt was originally owed.

- The type of financial or other product that incurred the debt, described in sufficient detail to distinguish among different products offered by the same creditor.

- The amount of the debt on the date it was first due and payable and, if different, the amount currently owing.

- The statement that the collection agency will provide a breakdown of the current amount owing, if requested.

- The following mandatory statement:

“Should you have any questions or would like further information regarding the current amount of your debt or the amount of your debt when it was first due and payable and, if applicable, would like a breakdown of the difference between those amounts, please contact our office at the number below as this information is available upon request.”

- The identity of the collection agency and collector who are demanding payment of the debt.

- The authority of the collection agency to demand payment of the debt.

- The information that if the debtor notifies the collection agency or collector that a particular method of communication causes the debtor to incur costs, or if the collection agency or collector otherwise becomes aware of that fact, the collection agency and collector are prohibited from subsequently contacting or attempting to contact the debtor using that method of communication.

- The contact information of the collection agency, including the full mailing address and toll-free telephone number and, where available, e-mail address and fax number. O. Reg. 460/17, s. 11.

(3) Despite subsection (1), a written demand for payment may be included with the written notice. O. Reg. 460/17, s. 11.

(4) The written notice may be sent by ordinary mail or by e-mail, except where the debtor has withdrawn his or her consent to the use of e-mail and provided a current address for ordinary mail. O. Reg. 460/17, s. 11.

FDR was hired for one purpose (to collect payment of a debt). Therefore, they are required to provide written notice before commencing collection activity. It appears that many debtors did not receive written notice from FDR.

NOTE: Thanks to Blair DeMarco-Wettlaufer of KINGSTON Data and Credit, a collection agent who has an excellent post on his blog explaining in detail how credit bureaus work and what can be reported. He notes that collection agencies are not required to send a notice if they don’t have a current address. Given that some of these debts are twenty years old, it’s likely that they don’t have a current address. However, if FDR is reporting to Equifax and TransUnion, they can check the credit bureaus to see if there is a current address on the bureau, and use that address to send the notice. Regardless, a creditor cannot report to the credit reporting agency until they have sent a notice and waited six days.

The City of Ottawa (specifically Joseph Muhini, the deputy city treasurer revenue) stated, “Prior to the debt being referred to the Collections Unit in Revenue Services, individuals are provided with an invoice, bill or a ticket and a deadline to pay the debt through regular channels.” While the City may have previously provided notice, I believe the law still requires any new collection agency to send out a fresh validation notice with their contact information.

It could also be argued that reporting a debt to Equifax or TransUnion is not an attempt to collect a payment of a debt. However, the City freely admits that reporting to the credit bureaus is a collection tactic:

“The most recent competitive process was completed in January, and one of the successful bids was Financial Debt Recovery (FDR). FDR has chosen credit bureau reporting as a collection method.”

So, clearly, reporting to Equifax and TransUnion is a collection method.

Limitation Periods

The City of Ottawa issued a memo stating that, “There is no statute of limitations for a conviction of a set fine.”

I’m not a lawyer, so they may be correct, but here’s what the law says:

The Provincial Offenses Act, section 76, says:

76 (1) A proceeding shall not be commenced after the expiration of any limitation period prescribed by or under any Act for the offence or, where no limitation period is prescribed, after six months after the date on which the offence was, or is alleged to have been, committed.

It appears that the limitation period may be six months. However, the Limitations Act also sets a basic limitation period of two years:

4 Unless this Act provides otherwise, a proceeding shall not be commenced in respect of a claim after the second anniversary of the day on which the claim was discovered

Again, I’m not a lawyer, but it appears that if the City wants to commence legal proceedings to collect unpaid parking tickets, they must commence legal proceedings either within six months or two years. It would appear that 20 years is well over the limitation period.

Credit bureau retention laws

The third issue is reporting very old debts to the credit bureau, some of which date back to 2003.

Under the Consumer Reporting Act of Ontario, a credit report cannot contain information about a debt that is more than seven years old.

Specifically, Section 9(3)(f) states that (again, bold by author):

(3) A consumer reporting agency shall not include in a consumer report….

(f) information regarding any debt or collection if,

(i) more than seven years have elapsed since the date of last payment on the debt or collection, or

(ii) where no payment has been made, more than seven years have elapsed since the date on which the default in payment or the matter giving rise to the collection occurred,

It appears that some of the debts were for traffic tickets from 2005, which is quite obviously more than seven years old.

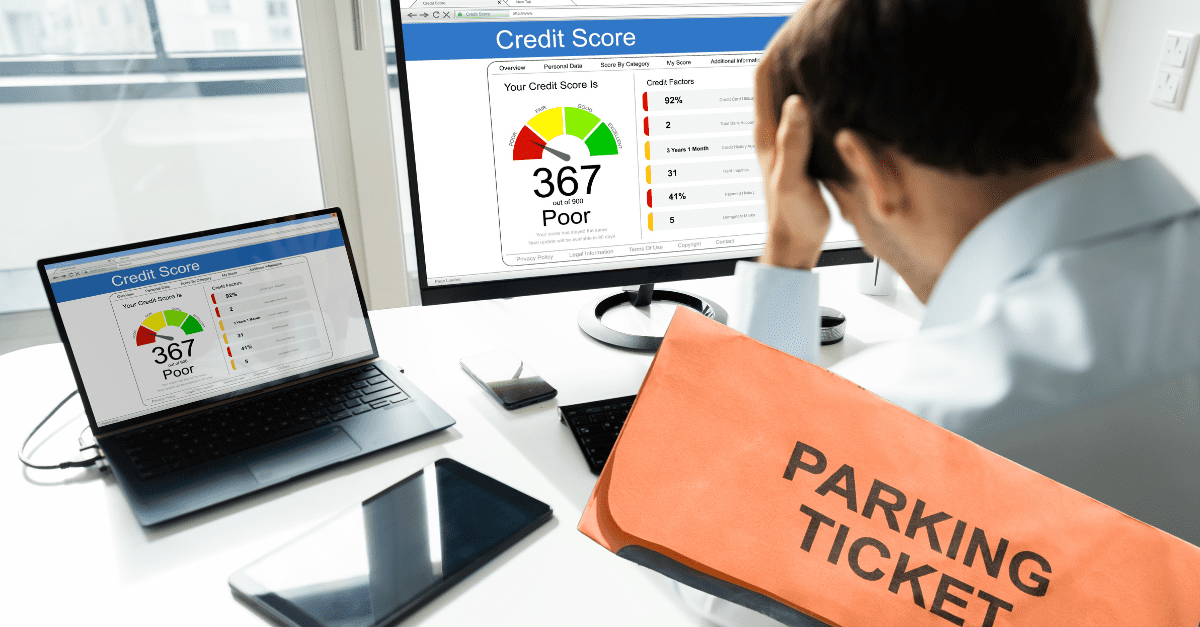

I spoke to a person today who attended university in Ottawa between 2001 and 2007, and his credit report just started reporting a debt from the City of Ottawa for $198 which appears to be from 2005.

He told me that last month, his credit score was 825. Today, because of this one small newly-reported debt, his credit score has dropped to 713.

(You may wonder how a credit score can drop by more than 100 points due to a small debt, but it’s a common occurrence).

The illegal reporting of an old debt has serious real-life consequences.

What if you are applying for a car loan or mortgage or you are renting an apartment? With a credit score of 825, qualification is easy. Qualification is more difficult if your credit score is 100 points lower. The situation worsens if your credit score starts at 700 and drops to 600. What was a “good enough” credit score may no longer be sufficient.

So, what’s my advice for people with old City of Ottawa debts on their credit report?

First, I suggest you contact the Mayor or your local representative to express your displeasure at these illegal collection tactics. If enough people complain, the politicians may make a change. Of course calling a politician may make you feel better but it won’t fix your credit report, so please read the final section below for my practical advice, but first, let’s address another important question:

Should you pay an old debt?

Second, if the debt is more than seven years old, may general advice is don’t pay it. You may think, “It’s only $200, I owe the money, I’ll pay it.” That’s understandable, but by paying the debt, you are admitting that you owe it, and you will restart the clock for how long the bad reference (an account sent to collection) can remain on your credit report. The seven-year period typically runs from your last payment. If the account is more than seven years old, the credit bureaus should not be reporting it. If you make a payment to FDR, it will potentially remain on your credit report for another seven years, negatively impacting your score in the long term.

In a memo, the City of Ottawa states that:

When all debts are collected by a private collection agency, the agency will report the item as paid through their regular reporting cycle and remove it from the credit report.

Is it true that FDR will “remove it from the credit report” when it is paid? I don’t know. Credit reports report history, so even if an old debt is paid, the fact that a debt was in arrears when it was paid may mean it will remain on your credit report and will impact your credit score. The City relies on FDR’s telling them the account will be removed from credit reports once it is paid. We will have to see if that is the case. That’s why my standard advice is to NOT pay a very old debt, because paying a debt that should not appear on your credit report may restart the seven-year-clock and negatively impact your credit score.

However, if FDR does agree, in writing, to remove all evidence of the debt from your credit report if you pay it, you can decide if paying the debt is worth it to restore your credit rating (which should not have been impacted in the first place).

Check your credit report

I advise you to immediately get your credit report directly from Equifax and TransUnion. I suggest you start with the free version of your credit report; it doesn’t include your credit score, but that’s not important now. Once you access your credit report, you can select the incorrect debt and immediately file a dispute. Your explanation will say, “debt from 2005, too old to display on a credit report, please remove,” or something to that effect.

By removing the debt from your credit report, it will no longer negatively impact your credit score.

If this old debt is your only debt, follow the instructions above, check back in a month to confirm that your credit report is updated, and you are good to go.

I will emphasize this point again, because this is the most important step you can take to protect your credit rating: Contact Equifax and TransUnion and dispute the debt. If the debt is older than seven years, it should not appear on your credit report. If Equifax and TransUnion receive enough complaints, they may take steps to correct the data proactively.

If you have many other debts, I suggest you contact our office, and we can review your credit report with you and determine if any other steps are required.